you’re probably grappling with an all-too-common question: “Can I file bankruptcy on a personal loan?” It’s a question that hangs heavy on the minds of many who find themselves buried under the weight of financial obligations.

You’re not alone, and the fact that you’re seeking answers is a testament to your resilience and determination.

Bankruptcy, a term often with negative connotations, is a legal process designed to offer a fresh start to those drowning in debt. It’s a complex tool, not to be used lightly, but in certain circumstances, it can provide a lifeline, a chance to wipe the slate clean and begin anew.

This blog article will get technical on personal loans, bankruptcy, and—most importantly—how the two relate to one another.

We’ll explore what personal loans are, the different types of bankruptcy—specifically Chapter 7 and Chapter 13—and how these types of bankruptcy affect personal loans.

We’ll also touch on the impact of bankruptcy on credit scores and provide some helpful strategies for rebuilding credit after bankruptcy.

Understanding these topics can be crucial in navigating your financial future, whether you’re considering filing for bankruptcy or simply looking to understand more about personal finance. Knowledge is power; in this case, it could be the key to regaining control of your financial life.

Stick with us, and let’s take this journey together. Remember, no question is too small or trivial when understanding your financial options and rights. So, let’s start by understanding more about personal loans.

Can I Declare Bankruptcy Due to a Personal Loan?

Table of Contents

Understanding Personal Loans

A personal loan can sometimes feel like a lifeline, a safety net that catches us when we stumble financially. But what happens when that lifeline begins to feel more like an anchor, pulling us deeper into the depths of debt? “Can I file bankruptcy on a personal loan?” is a question that might start echoing louder in our minds. To answer that, let’s first unpack a personal loan.

What is a Personal Loan?

A personal loan is a type of loan that can be used for a wide range of purposes. It could be for unexpected medical expenses, a long-overdue vacation, home renovations, or even to consolidate high-interest debts. It’s generally considered an unsecured loan, which means you don’t need to provide collateral (like your house or car) to get the loan.

How Does a Personal Loan Work?

When you apply for a personal loan, the lender will assess your creditworthiness primarily by looking at your credit score and verifying your income. If approved, you’ll receive a lump sum that you’ll repay in installments over a set period, typically with interest.

Interest Rates and Terms

Personal loan interest rates are very sensitive to borrowers’ credit histories. A lower interest rate is more likely to be provided to you if your credit score is higher. The repayment term (i.e., the time you have to pay back the loan) can also vary, often anywhere from one to seven years.

The Impact of Personal Loans on Your Credit

When handled responsibly, a personal loan can help improve your credit score. Prompt payments demonstrate to credit bureaus that you’re reliable, which can boost your score over time. However, the converse is true if payments are missed, which may harm your credit and make it more difficult to get credit in the future.

Can You File Bankruptcy on a Personal Loan?

Yes, you can file for bankruptcy on a personal loan. Personal loans, whether they are from credit unions, employers, friends, banks, or family, can be discharged in a bankruptcy case. They are considered unsecured debts, meaning there’s no collateral backing the loan, and therefore they can be included in a bankruptcy discharge.

However, the specific process and impact of discharging personal loans through bankruptcy depend on the type of bankruptcy you file—Chapter 7 or Chapter 13. As such, consulting with a bankruptcy attorney or a financial advisor is important to understand the implications and process fully.

Understanding personal loans is the first step to answering our initial question. But as we’ll see in the next sections, the relationship between personal loans and bankruptcy is influenced by many factors, including the type of bankruptcy filed. So let’s move on to explore those nuances.

The Concept of Bankruptcy

Bankruptcy. The word alone can feel heavy, almost daunting. When we’re struggling with debt, the question, “Can I file bankruptcy on a personal loan?” might arise. It’s a question that carries with it a sense of desperation and hope – hope for a fresh start. To understand what this means, let’s break down the concept of bankruptcy.

Can I Declare Bankruptcy Due to a Personal Loan?

What is Bankruptcy?

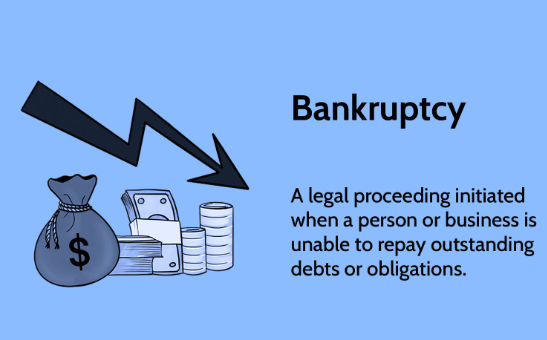

Bankruptcy is a legal process to relieve individuals or businesses that can’t repay their outstanding debts. The process begins when the debtor (the person who owes money) or the creditors (the entities to whom money is owed) file a petition in court. Bankruptcy gives the debtor a chance for a fresh start, but it’s not without its costs.

The Purpose of Bankruptcy

The basic objective of bankruptcy is to discharge debts, therefore releasing the debtor from legal responsibility to repay the obligations. This can provide a fresh financial start for individuals or businesses drowning in debt. The bankruptcy process also ensures that creditors are treated as fairly as possible. Remember, when you ask, “Can I file bankruptcy on a personal loan?” you ask if you can discharge that debt.

Types of Bankruptcy

Not all bankruptcies are created equal. The most common forms for individuals are Chapter 7 and Chapter 13. Chapter 7, “liquidation bankruptcy,” involves selling your non-exempt assets to pay back your creditors. On the other hand, Chapter 13, or “reorganization bankruptcy,” involves setting up a repayment plan to pay back your debts over three to five years. The type of bankruptcy you choose can affect which debts are discharged and how.

Implications for Borrowers

Filing for bankruptcy can offer a much-needed lifeline for those overwhelmed by debt. It can stop collection efforts and wage garnishments and potentially prevent eviction or foreclosure. However, it can also have serious consequences. If you’ve filed for bankruptcy, you may find it difficult to receive a loan, a mortgage, or even a job for the next seven to ten years.

Implications for Lenders

For lenders, a borrower filing for bankruptcy may not get the full repayment of the debt owed. However, the bankruptcy process ensures that all creditors are treated equitably, and in many cases, creditors may receive at least partial repayment of the debt.

When grappling with the question, “Can I file bankruptcy on a personal loan?” it’s essential to understand what bankruptcy means. It’s not a decision to be made lightly, but for some, it might be the best way to regain financial stability and start afresh. In the following sections, we’ll examine how different types of bankruptcy can affect personal loans.

Dischargeable Debts in Bankruptcy

The opportunity to get rid of or discharge some debts is a major perk of declaring bankruptcy. But what does that mean for your personal loans? Let’s dive into the concept of dischargeable debts and find out how this applies when you ask, “Can I file bankruptcy on a personal loan?”

Understanding Dischargeable Debts

The word “dischargeable debts” is used to describe the sorts of debt that may be discharged in bankruptcy. When a debt is discharged, you’re no longer legally required to pay it. This is one of the key ways bankruptcy can provide relief when you’re overwhelmed by financial obligations.

Types of Dischargeable Debts

Bankruptcy law allows a wide range of debts to be discharged. This typically includes credit card debt, medical bills, past-due utility bills, personal loans, and more. Not all debts, however, may be wiped out in bankruptcy. For example, student loans and tax debts are typically considered non-dischargeable, except in rare circumstances.

Personal Loans as Dischargeable Debts

The good news for those wondering, “Can I file bankruptcy on a personal loan?” Personal loans from a traditional lender, friends, or family are generally considered dischargeable debts. If you complete your bankruptcy process, your legal obligation to pay back these personal loans is eliminated.

Dischargeable Debts in Different Types of Bankruptcy

Whether a debt is dischargeable can also depend on the type of bankruptcy you file. In Chapter 7 bankruptcy, most dischargeable debts, including personal loans, can be completely wiped out. In Chapter 13 bankruptcy, you may still have to pay back a portion of your dischargeable debts through your repayment plan, depending on your income and the value of your assets.

The Impact of Discharging Debts

Discharging debts can provide significant relief, especially if you’re burdened with high-interest, unsecured debts like personal loans. However, it’s important to remember that while discharge eliminates your obligation to repay the discharged debts, it also impacts your credit score and future borrowing capabilities.

So, to answer the question, “Can I file bankruptcy on a personal loan?” – Yes, you generally can. But like all aspects of bankruptcy, it’s a decision that should be made with full knowledge of the implications and potential consequences.

A Closer Look at Chapter 7, Bankruptcy

Bankruptcy can seem complex, but understanding the specifics can make it less daunting. Chapter 7 bankruptcy, often called ‘liquidation bankruptcy,’ is one of the most common types. If you’re wondering, “Can I file bankruptcy on a personal loan through Chapter 7?” this section will provide some answers.

Can I Declare Bankruptcy Due to a Personal Loan?

Understanding Chapter 7, Bankruptcy

Chapter 7 bankruptcy is designed for debtors with little or no disposable income to pay off their debts. The process involves a court-appointed trustee who liquidates or sells your non-exempt assets to repay your creditors. The remaining dischargeable debts, including personal loans, can then be eliminated, giving you a fresh start.

Timeframe of Chapter 7, Bankruptcy

One of the attractions of Chapter 7 bankruptcy is its relatively quick timeframe. It typically takes about four to six months from the filing date to discharge your debts, including personal loans. This makes it a faster option than Chapter 13 bankruptcy, which can take three to five years to complete.

Impact on Personal Loans and Other Debts

In Chapter 7 bankruptcy, most unsecured debts, such as personal loans and credit card debts, are dischargeable. This means that once your bankruptcy process is complete, you’re no longer legally obligated to pay these debts. However, secured debts, like mortgages or car loans, are treated differently. If you wish to keep the property tied to a secured debt, you’ll usually need to continue paying for those loans.

Exempt and Non-exempt Assets

During Chapter 7 bankruptcy, some assets may be sold to repay your creditors. However, certain assets, known as exempt assets, are protected in bankruptcy. These typically include a certain amount of equity in your primary residence (the homestead exemption), a vehicle up to a certain value, necessary household goods, and retirement accounts, among others.

Understanding Chapter 13, Bankruptcy

If you have a steady income and are capable of repaying part or all of your obligations, Chapter 13 bankruptcy may be right for you. Unlike Chapter 7, which wipes out qualifying debts entirely, Chapter 13 involves creating a repayment plan to pay back your debts over three to five years.

The Repayment Plan

The repayment plan is the foundation of Chapter 13 bankruptcy. This court-approved plan is based on your income, expenses, and types of debt. It outlines how much you’ll pay to your creditors each month. Unsecured debts, like personal loans, are often paid a fraction of what is owed, while some secured debts may need to be paid in full, depending on your circumstances.

Impact on Personal Loans and Other Debts

In Chapter 13 bankruptcy, personal loans are classified as non-priority unsecured debts. This means they are often paid last; in many cases, only a portion of the personal loan debt is repaid. Any remaining balances on these debts are typically discharged at the end of your repayment plan.

How Chapter 13 Differs from Chapter 7

The main distinction between Chapter 13 and Chapter 7 bankruptcy lies in their approach to managing debts and assets. In Chapter 7, non-exempt assets are sold to repay debts, and most remaining debts are discharged. In Chapter 13, you keep all your assets but must repay your debts over time under the repayment plan. If you want to make up for missed mortgage or car loan payments and prevent foreclosure or repossession, choosing Chapter 13 may be more beneficial than Chapter 7, despite it taking a longer period of time.

The Aftermath of Chapter 13 Bankruptcy

Filing for Chapter 13 bankruptcy can have a negative effect on your credit, but it has a slightly shorter impact compared to Chapter 7. Your credit report will show your Chapter 13 bankruptcy filing for a period of seven years. Although it can be difficult to get new credit or personal loans during this period, it is still possible. Furthermore, as time passes and you make consistent payments on your repayment plan, the impact on your credit can lessen.

The Aftermath of Chapter 7 Bankruptcy

You may get rid of your dischargeable debts and start over with your finances if you apply for Chapter 7 bankruptcy. It is important to understand the long-term consequences of this choice. This type of bankruptcy remains on your credit report for ten years, which can make it more challenging to secure credit, including personal loans, in the future. However, don’t despair! After filing for bankruptcy, there are actions you may take to restore your credit, which we’ll go over in a later section.

A Closer Look at Chapter 13, Bankruptcy

When filing for bankruptcy on a personal loan, it’s important to understand all your options. Reorganization bankruptcy, sometimes referred to as Chapter 13, is a separate kind of bankruptcy from Chapter 7 and operates in a somewhat different way. Let’s examine a few of the important features.

Can I Declare Bankruptcy Due to a Personal Loan?

Can You File Bankruptcy on a Personal Loan Using Chapter 13?

Absolutely. However, remember that this option involves a commitment to a long-term repayment plan and will significantly impact your credit. Like any major financial decision, it’s best to consult a financial advisor or attorney to understand all the implications.

Comparing Chapter 7 and Chapter 13, Bankruptcy

Making the significant choice to file for bankruptcy may have long-term consequences for your financial future. Understanding the distinctions between Chapter 7 and Chapter 13 bankruptcy is essential when it comes to personal loans. To assist you in navigating the complexity of each, I’ve broken out the important comparative points below.

Purpose

Both Chapter 7 and Chapter 13 bankruptcy aim to aid in your financial recovery, although they achieve different objectives. Those who have a low income and mounting obligations can consider Chapter 7. Chapter 13 bankruptcy, on the other hand, is designed for those who have a steady income and are capable of paying back some of their obligations.

Process

In Chapter 7, non-exempt assets are liquidated to pay off as much debt as possible, and then most remaining debts are discharged. In Chapter 13, there’s no liquidation. Instead, you enter a three to five-year repayment plan to pay back all or a portion of your debts. Any remaining balances on certain debts, like personal loans, are discharged at the end of the plan.

Timeframe

Chapter 7 bankruptcy tends to be quicker, usually taking four to six months to complete. Conversely, Chapter 13 bankruptcy is a long process due to the repayment plan, which lasts three to five years.

Impact on Personal Loans

Personal loans are regarded as obligations that may be discharged under Chapters 7 and 13. In Chapter 7, these debts can be wiped out entirely, while in Chapter 13, they are often paid partially through the repayment plan, with the remainder discharged at the end.

Effect on Credit

Both types of bankruptcy will have a substantial impact on your credit. Unlike Chapter 13, Chapter 7 stays on your credit record for seven years. However, don’t be disheartened. With good financial habits, you can rebuild your credit over time.

Retention of Assets

One of the stark differences is how they treat your assets. In Chapter 7, some of your assets may be sold to repay debts. In Chapter 13, you can keep all your assets but must pay back your debts via the repayment plan.

The question “Can I file bankruptcy on a personal loan?” is answered with a resounding yes, whether you’re considering Chapter 7 or Chapter 13. But remember, bankruptcy is a significant decision with lasting impacts. It’s always recommended to seek advice from financial experts or legal counsel to fully understand the repercussions and to explore all possible alternatives.

Can I Declare Bankruptcy Due to a Personal Loan?

How Bankruptcy Affects Your Credit Score

As we navigate the question, “Can I file bankruptcy on a personal loan?” It’s critical to comprehend how bankruptcy impacts your credit rating and future loan applications. Bankruptcy will significantly impact your creditworthiness, but it’s not a life sentence, and there are ways to rebuild your credit over time. Here’s what you should know:

Immediate Impact

Your credit score will be significantly and immediately lowered if you file for bankruptcy. It’s seen as a last resort and a clear indication that you’ve been unable to meet your financial obligations.

Long-Term Effects

There will be long-lasting effects on your credit score after declaring bankruptcy. For Chapter 7 bankruptcy, it stays for ten years, while for Chapter 13, it stays for seven years. Any lender reviewing your credit report will see your bankruptcy filing for that period, which could influence their decision on whether to lend to you.

Loan Applications

When bankruptcy is on your credit report, you may find it more difficult to secure loans, including personal loans. If lenders determine that you pose too great of a risk, they may not approve your loan application or may only do so with less-than-ideal conditions, such as a higher interest rate.

Credit Score Recovery

While bankruptcy will initially lower your credit score, you can rebuild it immediately. You can do this by making timely payments on any new credit, lowering your credit utilization, or obtaining a credit-builder loan. It’s a process that requires discipline and patience, but with time, your credit score can recover.

Income and Loan Approval

Despite the negative impact on your credit score, your income will still be a factor when applying for loans after bankruptcy. A stable income demonstrates your ability to repay the loan, which might make lenders more willing to approve your loan application, even with bankruptcy on your record.

Bankruptcy is a serious financial step with long-lasting implications, but it is also a path to a fresh start. Remember, the goal is to relieve unbearable debt, including personal loans, and set yourself on a path toward financial recovery.

Rebuilding Your Credit After Bankruptcy

If you’ve found yourself asking, “Can I file bankruptcy on a personal loan?” and have decided to go through with it, having a plan for rebuilding your credit post-bankruptcy is crucial. This process won’t be overnight, but it’s possible and is the key to your financial recovery. Here’s how you can start:

Be Timely with New Credit

One of the most influential factors in your credit score is your payment history. Keep up with timely bill payments after bankruptcy. Not only do you have to pay off your loans and credit cards, but also your rent, electricity, and mobile phone bill. Timely payment demonstrates to potential lenders that you’re responsible with credit.

Lower Your Credit Utilization

Utilization of credit is the percentage of available credit that is actually used. Keeping your credit usage low (ideally below 30%) is a good practice, as high utilization can signal to lenders that you’re reliant on borrowed money.

Consider a Credit-Builder Loan

Credit-builder loans are available from several financial institutions to those who need to repair their credit. The borrowed funds are placed in escrow with the lender until the loan is repaid. It might seem counterintuitive, but it’s a useful tool to demonstrate your reliability as a borrower.

Get a Secured Credit Card

A secured credit card is another tool to help rebuild credit. It requires a cash collateral deposit that becomes the credit line for that account. This might be a good strategy to raise your credit score if you utilize it carefully.

Monitor Your Credit Report

Monitor your credit report closely to track your progress and spot any errors. Every year, you’re entitled to a free report from the three major credit bureaus. Make use of these to ensure all the information is correct and up-to-date.

Remember, bankruptcy, including the discharge of personal loans, is not the end. It’s a chance to reset, learn from the past, and build a more stable and secure financial future. You’ll see your credit score improve with patience, discipline, and consistent effort.

Can I Declare Bankruptcy Due to a Personal Loan?

Income Verification and Loan Approval After Bankruptcy

It’s common for people to wonder, “Can I file bankruptcy on a personal loan?” If you’ve had to take that step and are now rebuilding, it’s essential to understand the role income verification plays when applying for a new loan after bankruptcy. A stable income can significantly enhance your chances of approval. Here are some key points to understand:

Why Income Verification is Important

After bankruptcy, your income becomes an important indicator of your ability to repay a loan. Lenders want assurance that you have a steady income source to meet your loan obligations. Income verification helps provide this assurance.

How Income Verification Works

To prove your income, you’ll probably be requested to provide pay stubs, tax documents, or bank records. These details help lenders evaluate your capacity to repay the loan and decide how much money they will grant you.

The Advantage of a Stable Income

A stable income demonstrates your ability to repay the loan and financial stability, making you a less risky borrower in the eyes of lenders.

Increased Chances of Loan Approval

With a stable income, you can verify you stand a higher chance of loan approval post-bankruptcy. While your past bankruptcy might put some lenders on edge, a steady income helps tilt the balance in your favor.

The Role of Income in Determining Interest Rates

While your bankruptcy and credit score will largely influence the interest rates offered, your income can also play a part. A higher income can sometimes help secure a lower interest rate, making the loan more affordable.

Every step counts when you’re on the path to financial recovery after bankruptcy. Income verification may seem like just another hoop to jump through, but it’s crucial to demonstrate your creditworthiness to potential lenders. You may better prepare for the loan application process and raise your chances of acceptance by being aware of its significance.

Can I Declare Bankruptcy Due to a Personal Loan?

Frequently Asked Questions ( FAQS )

Can a personal loan be written off in bankruptcy?

Through filing for bankruptcy, unsecured personal loans may be dismissed or canceled. Loans that are not secured by your personal property are known as unsecured loans. Also eligible for discharge are personal debts taken out from friends, family, or employers.

How long after a personal loan can I file for bankruptcy?

It’s advisable to hold off on filing for at least 90 days after taking out payday loans or making any significant expenditures. This is so that a trustee or court won’t be suspicious of your transactions and less likely to approve your bankruptcy.

What loans are not covered by bankruptcy?

Non-dischargeable debt refers to a class of loan obligations that cannot be discharged in bankruptcy. Student loans, municipal taxes, taxes (the majority of which are state and federal), funds used to pay those taxes using a credit card, child support payments, and any alimony are among these obligations.

Do loans go away with bankruptcy?

Debt related to student loans may be difficult, but not impossible, to discharge in bankruptcy. Both federal and private student debts are dischargeable in bankruptcy. Because of the negative effects bankruptcy may have on your credit, as well as the expenses and time required to file for bankruptcy, it’s sometimes seen as a last resort.

Which type of personal bankruptcy filing forgives most of your debt?

Your debt is mostly discharged in Chapter 7 bankruptcy.

Conclusion: Can I file bankruptcy on a personal loan – Recap?

It’s been a journey exploring the question, Can I Declare Bankruptcy Due to a Personal Loan? ” and navigating the complexities of bankruptcy. We’ve covered a lot of ground, and it’s important to remember a few key points:

Dischargeable Debts: Personal loans and other debts like credit card bills and medical expenses are considered dischargeable in bankruptcy. This means they can be wiped clean, giving you a fresh start.

Chapter 7 Bankruptcy: Chapter 7 bankruptcy, sometimes referred to as “liquidation bankruptcy,” entails selling your non-exempt assets to pay off your obligations. It’s a relatively quick process that can take about four to six months to complete.

Chapter 13 Bankruptcy: This type of bankruptcy, often called “reorganization bankruptcy,” allows you to keep your property and pay off your debts over time through a court-approved repayment plan.

Impact on Credit Score: A bankruptcy filing might remain on your credit report for up to ten years. As a consequence, your future loan applications can suffer.

Rebuilding Credit: You may take actions to raise your credit score even after filing for bankruptcy, such as paying back new credit on time, reducing your credit utilization, or obtaining a credit-builder loan.

Income Verification: Post-bankruptcy, lenders greatly emphasize your income when considering you for a loan. Having a stable, verifiable income can increase your chances of loan approval.

Filing for bankruptcy on a personal loan is a decision that should be made with careful thought and advice from a qualified professional. It can relieve overwhelming debt, but it also comes with challenges. The journey to financial recovery may be long, but with the right approach, it’s certainly possible. Take each step cautiously, make informed decisions, and remember: every setback is a setup for an even greater comeback.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.